Here’s an article on “What is a Life Insurance Beneficiary and How Do You Choose One?” designed for a life insurance website:

What is a Life Insurance Beneficiary and How Do You Choose One?

Life insurance provides financial security for your loved ones in the event of your passing, but choosing the right beneficiary is just as important as selecting the policy itself. A life insurance beneficiary is the person, entity, or organization that will receive the death benefit when the policyholder passes away. Understanding the role of a beneficiary and carefully considering who to designate can help ensure that your financial legacy is distributed according to your wishes.

In this article, we’ll explain what a life insurance beneficiary is, the different types of beneficiaries, and how to choose the right one for your situation.

What is a Life Insurance Beneficiary?

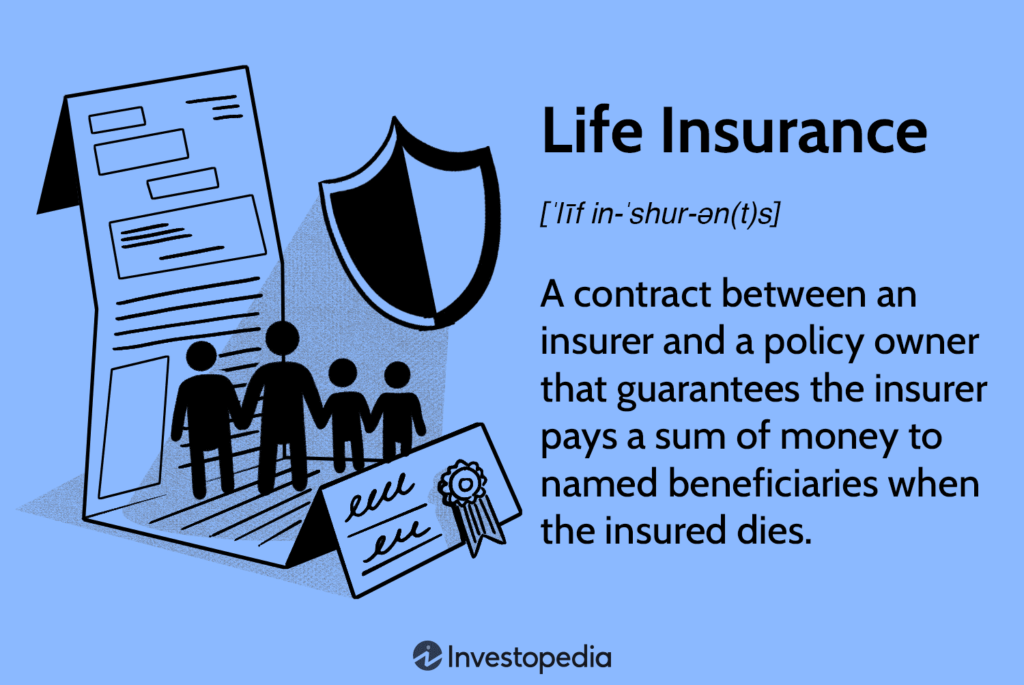

A beneficiary is the person, people, or entity designated to receive the payout from your life insurance policy when you pass away. This benefit is typically tax-free and can be used by the beneficiary for any purpose, such as covering living expenses, paying off debts, funding education, or saving for retirement.

When purchasing a life insurance policy, you’ll be asked to name one or more beneficiaries. You can update or change these beneficiaries at any time, which is a key feature of life insurance.

Types of Life Insurance Beneficiaries

There are generally two types of beneficiaries you can designate: primary and contingent.

1. Primary Beneficiary

- The primary beneficiary is the first person or entity entitled to receive the death benefit from your policy. If you pass away, the primary beneficiary will receive the full benefit, assuming they are still alive.

- Examples: A spouse, children, parents, or a trust you’ve established.

2. Contingent Beneficiary

- The contingent beneficiary is the secondary person or entity who will receive the death benefit if the primary beneficiary is deceased or cannot be located. It’s essentially a backup to ensure the benefit goes to someone if the primary beneficiary is unable to claim it.

- Examples: A sibling, close friend, charity, or another relative.

Who Can Be a Life Insurance Beneficiary?

You can name virtually anyone as a beneficiary, but there are some important considerations when making your decision. Here are some common beneficiaries:

1. Family Members

- Spouse: Many people choose their spouse as the primary beneficiary to ensure their partner’s financial well-being.

- Children: Parents may choose to name their children as primary beneficiaries. In cases where the children are minors, a guardian may be appointed to manage the funds until they come of age.

- Parents or Siblings: In the absence of a spouse or children, parents or siblings may be named beneficiaries, especially if they rely on your support.

2. Trusts

- Trusts: Some policyholders choose to designate a trust as their beneficiary, which allows the death benefit to be managed by a trustee according to the terms of the trust. This can be beneficial for estate planning, ensuring that the funds are used in a specific manner, such as for education or medical expenses.

3. Charities or Organizations

- Charities: You can designate a charity or nonprofit organization as your beneficiary, ensuring that your life insurance proceeds go to a cause you care about.

4. Business Entities

- Business Partners: In the case of business owners, the business itself or a business partner might be designated as a beneficiary, particularly for buy-sell agreements or business protection.

How to Choose a Life Insurance Beneficiary

Choosing the right life insurance beneficiary is a decision that should align with your long-term goals and personal circumstances. Here are several factors to consider when naming a beneficiary:

1. Evaluate Your Family Dynamics

- Spouse: If you’re married, it’s common to name your spouse as the primary beneficiary. This ensures they will have the financial means to maintain their lifestyle, cover debts, and take care of any dependents.

- Children: If you have children, consider how you want the death benefit distributed among them. If they are minors, you may need to appoint a guardian or set up a trust to manage the funds on their behalf.

2. Consider Financial Needs

- Dependents: Think about who depends on you financially. This could include a spouse, children, elderly parents, or even siblings. Choose beneficiaries who would be most impacted by your passing and could benefit from the life insurance payout.

- Debts: If you have significant debts, consider how your life insurance death benefit might help your beneficiaries cover these financial obligations. A policy may provide much-needed funds to help cover outstanding mortgages, student loans, or other liabilities.

3. Choose a Contingent Beneficiary

- Backup Option: It’s essential to name a contingent beneficiary in case your primary beneficiary is unable to claim the death benefit (for example, if they pass away before you do). This ensures your death benefit goes to the next person in line without delays or complications.

4. Consider Tax Implications

- Tax Benefits: Life insurance benefits are generally tax-free, but it’s still important to consult with a financial advisor to ensure that your beneficiary designation aligns with your overall estate planning goals. For example, naming a trust as your beneficiary can help you control how the funds are distributed and may have tax advantages.

5. Review and Update Your Beneficiaries Regularly

- Life Changes: Your life circumstances will change over time—marriage, divorce, births, deaths, and financial changes all impact your beneficiary choices. Review your policy regularly to ensure that your beneficiary designations reflect your current wishes.

- Divorce: If you divorce, it’s essential to update your beneficiary designations. In many states, ex-spouses may still be considered a beneficiary unless you officially change it.

How to Update Your Beneficiary Designation

It’s easy to update your beneficiary information, and it’s important to keep your designation current. Here’s how:

- Contact Your Life Insurance Provider: Reach out to your insurer to request a beneficiary change form. This can often be done online or by phone.

- Complete the Form: Fill out the necessary details, such as the name of the beneficiary, relationship to you, and contact information.

- Submit the Form: Submit the form to your insurance provider for processing. Keep a copy for your records.

- Confirm the Update: Follow up with your insurer to ensure the beneficiary update has been processed correctly.

Final Thoughts

Choosing a life insurance beneficiary is one of the most important decisions you’ll make when purchasing a policy. It’s essential to carefully consider who will benefit from your life insurance payout and how the funds will be used. Whether you choose family members, a trust, a charity, or a business partner, the key is to ensure your death benefit is directed according to your wishes.

By regularly reviewing and updating your beneficiary information, you can ensure that your loved ones or causes you care about are well taken care of after you’re gone. Always consult with a financial advisor or insurance professional if you need guidance in choosing the right beneficiary or managing your life insurance policy effectively.

This article provides a comprehensive overview of life insurance beneficiaries and offers guidance on how to choose the right one. If you are unsure about who to designate, consulting with an insurance professional can help you make the best decision for your specific needs.

Leave a Reply